Crypto Stocks Crushed as Nasdaq Correction Triggers $17T Market Downturn

A severe market correction has battered crypto-related equities as the Nasdaq enters official correction territory amid a broader $17 trillion global market rout. The selloff reflects renewed macroeconomic concerns and investor risk-off sentiment, with cryptocurrency holdings and blockchain company stocks experiencing disproportionate losses compared to traditional equity markets.

Overview

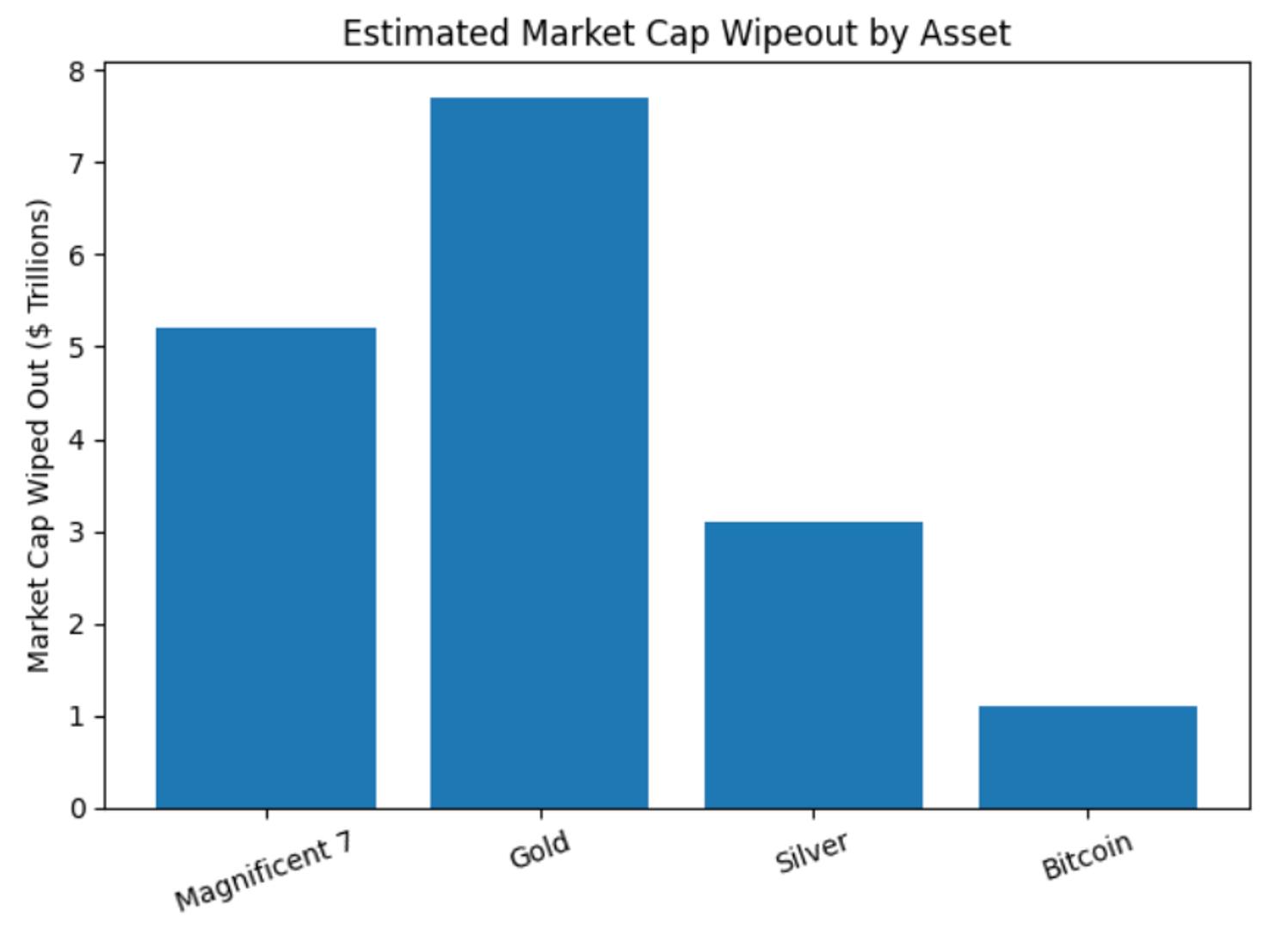

Global financial markets entered a significant correction phase in late March 2026, with the technology-heavy Nasdaq index officially crossing the 10% decline threshold from recent highs—the traditional marker for correction territory. This broader market downturn, characterized by a staggering $17 trillion in total value erosion across global asset classes, has disproportionately impacted cryptocurrency-related stocks and digital asset equities. Major cryptocurrency exchanges, blockchain infrastructure companies, and crypto-adjacent fintech firms have experienced sharper declines than their non-crypto counterparts, signaling that digital assets remain the market's most volatile and risk-sensitive sector.

The correlation between traditional equity selloffs and crypto market weakness has become increasingly pronounced, challenging the long-held narrative that cryptocurrency operates as a hedge against broader market downturns. Investors holding positions across crypto stocks, blockchain equities, and digital asset companies have faced severe losses as risk-off sentiment swept through institutional and retail portfolios alike. This market correction represents a critical inflection point for the cryptocurrency industry, raising questions about valuations, market maturity, and the sector's resilience during periods of macroeconomic stress.

The $17 trillion in global market losses encompasses equities, bonds, commodities, and alternative assets across developed and emerging markets. Within this broader context, cryptocurrency and crypto-stock valuations have contracted at rates significantly exceeding general equity market declines, reflecting both leverage unwinding in the sector and fundamental reassessment of crypto asset valuations. The divergence between crypto and non-crypto market performance underscores the elevated risk profile investors assign to digital asset companies and blockchain-related equities.

Background

The path to this market correction involved multiple contributing factors that accumulated throughout early 2026. Persistent inflation concerns in major developed economies, coupled with cautious central bank policy signals regarding interest rate trajectories, created headwinds for risk assets. The U.S. Federal Reserve and other major central banks maintained hawkish policy stances longer than many investors anticipated, pressuring valuations across growth-oriented and technology-intensive sectors—precisely where most crypto-related companies are concentrated.

Cryptocurrency markets had experienced a substantial bull run extending from late 2024 through early 2026, driven by institutional adoption narratives, favorable regulatory developments in several jurisdictions, and technical momentum. Bitcoin and Ethereum reached multi-year highs, with altcoin markets experiencing even more dramatic appreciation. This extended rally created stretched valuations and significant positioning in leveraged trading vehicles, derivatives markets, and speculative retail accounts. The concentration of leverage in crypto markets—through margin trading, futures, and structured products—amplified both the upside during the bull market and the downside during the correction.

Macroeconomic headwinds intensified as March 2026 progressed. Geopolitical tensions, energy market volatility, and weaker-than-expected economic data from several major economies triggered a broader reassessment of growth expectations. Risk assets across all categories faced selling pressure, but crypto markets proved most vulnerable due to their existing leverage, narrow holder bases in certain segments, and sensitivity to sentiment shifts. The withdrawal of retail investor enthusiasm, often a significant driver of crypto rallies, coincided with institutional profit-taking after months of gains.

Regulatory uncertainty in several key jurisdictions also contributed to the selloff. Proposed regulations regarding stablecoin reserves, cryptocurrency exchange operations, and institutional custody arrangements created headlines and triggered concerns among crypto market participants. While some regulatory developments could ultimately prove favorable for market maturity, the near-term impact was decidedly negative as investors sold first and asked questions later.

Key Developments

The Nasdaq's entry into correction territory—marked by a 10%+ decline from peak—served as a psychological and technical threshold that triggered additional selling. Major technology companies, including those with significant crypto exposure or blockchain operations, experienced substantial share price declines. Coinbase, the largest U.S. cryptocurrency exchange operator and a bellwether for institutional crypto adoption, faced particularly severe selling pressure as investors reassessed the valuation multiples commanded by crypto-focused equities.

Beyond pure-play crypto companies, traditional financial institutions with significant cryptocurrency divisions also felt the impact. Banking stocks exposed to cryptocurrency lending, crypto asset custody, and digital asset trading faced investor concerns about counterparty risk and potential credit quality deterioration. The memory of the 2022-2023 crypto winter, when several crypto-focused lending platforms collapsed, influenced investor behavior and risk appetite for crypto-exposed traditional finance firms.

Leveraged positions throughout crypto derivatives markets began unwinding rapidly as margin requirements increased and liquidation cascades triggered further selling. Futures markets across major cryptocurrency pairs experienced significant volatility, with billions of dollars in leveraged long positions liquidated within short timeframes. These mechanical liquidations amplified downward price momentum and contributed to the severity of the correction in spot prices.

Cryptocurrency prices themselves experienced double-digit percentage declines, with some altcoins experiencing even sharper losses. Bitcoin, traditionally the most stable cryptocurrency, declined significantly below key technical support levels, signaling capitulation among holders. Ethereum and other large-cap cryptocurrencies fell in line with Bitcoin, demonstrating that the correction affected the entire digital asset ecosystem rather than isolated segments.

Regional differences in regulatory approaches became apparent as various jurisdictions responded to the market turmoil. Some countries accelerated cryptocurrency regulatory frameworks, while others took more cautious stances. The uncertainty around regulatory direction created additional volatility and contributed to the extended nature of the selling.

Market Impact

The broader impact of this correction extends well beyond cryptocurrency and crypto stocks. The $17 trillion in global market losses affected traditional equities, bond markets, commodities, and alternative investments simultaneously. This correlational breakdown between asset classes—where everything declined together—limited portfolio diversification benefits and forced risk management actions across institutional portfolios.

Cryptocurrency market capitalization contracted by hundreds of billions of dollars within the span of days, erasing months of gains for long-term holders. Retail investors who had accumulated positions during the bull market faced substantial unrealized losses, potentially triggering behavioral responses including capitulation selling and reduced risk appetite. Sentiment indicators across cryptocurrency social media platforms and forum discussions shifted dramatically from optimistic to pessimistic.

Institutional investors reduced their cryptocurrency allocations as risk management protocols triggered rebalancing requirements. Endowments, sovereign wealth funds, and pension plans that had increased crypto exposure as part of diversification strategies faced pressure to trim positions and reallocate to less volatile assets. This institutional selling, while perhaps modest in absolute terms, had outsized impact on crypto markets due to their relatively smaller size compared to traditional equity markets.

Crypto lending platforms and protocols that had expanded aggressively during the bull market faced stress as collateral values declined and withdrawal requests increased. Decentralized finance (DeFi) platforms experienced higher levels of liquidations as collateralized debt positions automatically closed at lower asset prices. Some smaller crypto lenders and trading platforms raised concerns about potential solvency given the rapid market deterioration.

The impact on crypto stock valuations proved particularly severe. Companies whose business models depend on high cryptocurrency prices and trading volumes—such as mining operations, exchange platforms, and payment processors—saw share prices compress dramatically. Enterprise value-to-revenue multiples that had expanded significantly during the bull market contracted swiftly as investors reassessed normalized earnings potential during bear market conditions.

Employment in cryptocurrency companies faced pressure as several firms announced workforce reductions in response to deteriorating business conditions. This second-order effect of the market correction could persist longer than the initial price declines, affecting recruiting, retention, and innovation in the sector. However, previous cycles showed that downturns also sparked consolidation and the emergence of stronger, better-capitalized competitors.

Risks and Considerations

Several significant risks merit attention as this correction unfolds. Contagion risk across cryptocurrency lending markets and trading platforms remains elevated. If leveraged entities experience margin calls they cannot meet, the resulting defaults could cascade through interconnected platforms. Regulators and market observers remain vigilant for signs of systemic stress similar to the 2022-2023 period.

The correlation between traditional markets and cryptocurrency markets, which had weakened during the 2024-2026 bull run, has re-strengthened during this correction. This suggests that cryptocurrency's diversification benefit—a key selling point for institutional adoption—may be limited during periods when it matters most. Investors who allocated to crypto assets specifically to hedge equity market risk face the disappointing discovery that this hedge proved ineffective.

Liquidity risk in cryptocurrency markets represents another consideration. While large-cap cryptocurrencies like Bitcoin and Ethereum maintain reasonable liquidity, significant portions of the crypto market consist of lower-volume altcoins where large orders can move prices significantly. If a major holder or leveraged entity attempts rapid liquidation, further price dislocations could emerge. Liquidity crisis scenarios in crypto derivatives markets remain possible if volatility persists.

Regulatory risk intensified during the downturn. Governments and regulators may use market stress as justification for restrictive regulatory frameworks intended to prevent future volatility. While prudent regulation could ultimately benefit market maturity, overly restrictive approaches could impair innovation and competitiveness in cryptocurrency development. The outcome of regulatory deliberations over coming months remains uncertain.

Valuation risk considerations apply to both overshooting on the downside and the sustainability of any recovery. Cryptocurrency valuations have historically experienced significant oscillation—from bubble peaks to capitulatory lows—making it difficult to establish fundamental value. The current correction could represent fair repricing, or it could represent overshooting, or elements of both. Investors lack reliable frameworks for assessing fair value, particularly in nascent cryptocurrencies with limited cash flows and abstract value propositions.

Psychological and behavioral risks should not be underestimated. Retail investor panic selling, forced liquidations from margin positions, and the psychological impact of significant unrealized losses can create downward spirals. However, historically these periods have also created buying opportunities for long-term investors with contrarian views and adequate capital.

What to Watch

Market observers should closely monitor cryptocurrency exchange reserves and outflow patterns. Significant inflows into exchange cold wallets by major holders could suggest capitulation and potential market bottom formation. Conversely, continued outflows might indicate ongoing selling pressure from remaining bull-positioned investors.

Leverage metrics across cryptocurrency derivatives markets warrant careful observation. The Funding rate (cost of maintaining leveraged positions) and the notional value of open interest in futures markets provide indicators of positioning and potential further liquidation cascades. When funding rates turn deeply negative, markets often near capitulatory bottoms.

Regulatory developments in major jurisdictions—the United States, Europe, Singapore, and others—will significantly influence recovery trajectories. Clarity on stablecoin regulations, exchange licensing, and institutional custody frameworks could either accelerate recovery (if positive) or extend downturn (if restrictive). Legislative calendars and regulatory agency actions should be monitored closely.

Crypto stock valuations relative to cryptocurrency price movements represent another key metric. If crypto stock declines significantly exceed cryptocurrency price declines, it suggests the equity market is pricing in structural damage to business models. Conversely, divergence in the other direction could indicate contrarian opportunity for crypto equity investors.

Institutional adoption trends will largely determine crypto's trajectory. If institutions maintain allocation levels despite the downturn, market recovery could be sustained. If institutional liquidation accelerates, markets could face extended pressure. Central bank digital currency (CBDC) development progress should also be monitored as potential long-term catalyst for or competitor to decentralized cryptocurrencies.

Macroeconomic data—particularly inflation readings, employment statistics, and central bank policy signals—will heavily influence risk asset recovery broadly. If macroeconomic conditions stabilize, crypto should participate in broader risk-asset rebounds. However, if economic headwinds intensify, crypto's risk-sensitive nature could result in further relative underperformance.

Conclusion

The correction of 2026, characterized by a $17 trillion global market rout and the Nasdaq's entry into official correction territory, has proven particularly damaging to cryptocurrency markets and crypto-related equities. The disproportionate impact on digital assets reflects both the leverage embedded in crypto markets and the sector's heightened sensitivity to macroeconomic conditions and sentiment shifts. What was once positioned as an uncorrelated alternative asset class has demonstrated strong correlation with risk assets during periods of market stress.

However, historical cryptocurrency market cycles suggest that corrections, even severe ones, have ultimately given way to renewed bull markets and new all-time highs. The 2022-2023 bear market seemed catastrophic in real-time but eventually resolved into an even stronger 2024-2026 bull run. Current investors face the challenge of distinguishing between cyclical corrections within a longer-term bull market and potential structural downturn reflecting fundamental reassessment of cryptocurrency valuations.

The path forward depends significantly on macroeconomic resolution, regulatory clarity, and whether cryptocurrency markets can demonstrate genuine maturity by avoiding cascading failures and systemic events. For long-term believers in cryptocurrency technology and adoption narratives, the correction likely represents a buying opportunity. For those with shorter time horizons, patience and selective entry points become paramount.

The crypto industry should emerge from this correction with valuable lessons about the risks of excessive leverage, the importance of market infrastructure resilience, and the ongoing need for regulatory clarity. While the near-term outlook remains uncertain, cryptocurrency's fundamental value proposition—decentralized, censorship-resistant digital money and smart contract platforms—remains intact. The market downturn, though painful for current holders, may ultimately strengthen the sector by eliminating excess speculation and forcing sustainable business model development.

Investors and market participants should remain vigilant about emerging risks, attentive to regulatory developments, and prepared for the extended volatility that typically characterizes cryptographic asset market cycles. The $17 trillion market rout will eventually become historical context for the next chapter of cryptocurrency's evolution.

Original Source

CoinDesk